54% of Homeowners Can't Afford a Major Home Repair

Groundworks asked 2,000+ people if they could afford a major home repair. Find out how emergency preparedness has changed during COVID-19.

The coronavirus pandemic has disrupted household finances. If there’s an unexpected home repair, the situation can quickly go from bad to worse. A home’s livability and household safety could be at stake, but immediate repairs could be out of reach for many households.

A recent Groundworks survey asked homeowners across the country about how prepared they were for a major home repair. The results reveal that more than half of all homeowners do not have enough savings to cover a major home repair.

How Many Homeowners Can Afford a Major Home Repair?

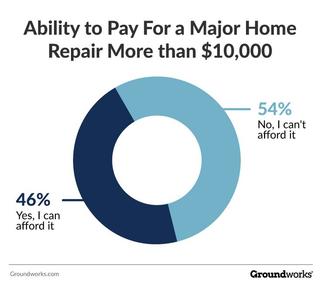

Groundworks asked more than 2,000 homeowners about how prepared they were to deal with a major home repair that costs $10,000 or more. To get accurate results, the survey included a broad sample of ages and locations. The survey results reveal that as of October 2020, 54 percent of homeowners do not have the savings needed to afford a major home repair.

Ability to Pay For a Major Home Repair More than $10,000

- No, I can’t afford it: 54%

- Yes, I can afford it: 46%

Who Is More Likely to Be Unable to Afford Large Home Repairs?

Our survey revealed two key segments that are more at risk of being unable to afford major home repairs: women and young homeowners.

It may not come as a shock that young homeowners are less prepared for a major home repair bill. Because of their age, these homeowners have had less time to accumulate savings. Plus, as new homeowners, they could have leveraged more of their resources to secure a mortgage. In comparing young homeowners with older ones, there’s about a 10 percent difference in their preparedness for major repairs.

Young Homeowners (age 25-34)

- No, I can’t afford it: 65%

- Yes, I can afford it: 35%

Older Homeowners (age 55-64)

- No, I can’t afford it: 54%

- Yes, I can afford it: 46%

Our survey also shows that women homeowners are less likely to be able to afford major repairs than men. With about a seven percent difference between the genders, the disparity could hint at underlying financial circumstances such as the gender pay gap.

Women’s Ability to Pay For a Major Home Repair

- No, I can’t afford it: 58%

- Yes, I can afford it: 42%

Men’s Ability to Pay For a Major Home Repair

- No, I can’t afford it: 51%

- Yes, I can afford it: 49%

What Types of Major Home Repairs Could Homeowners Face?

On average, homeowners spend $4,958 per year on home repairs and improvements. However, there are some circumstances where a homeowner could face a larger repair bill.

Some large repairs can be the result of unexpected damage. Whether it’s a tree falling on a roof or there’s an unexpected basement flood, unforeseen events can cause high repair bills. According to FEMA, just one inch of water can result in $26,807 worth of damages. If floodwaters rise to one foot, the financial toll would be $72,162.

Major repairs can be a part of routine maintenance. The lifecycle of certain home features can mean that large home repair bills occur every few years. For example, roofs made of asphalt shingles need to be redone every 20 years, and central air systems typically last 10 to 15 years.

Other large repairs are a way to interrupt an ongoing damage cycle. For example, the unrelenting damage caused by a termite infestation can destroy a home from the inside out. Some regions face more of a threat, and within the next two decades, half of all homes in Florida will be at risk for termite damage. Extermination and major repairs may be required to preserve structural stability.

Major repairs can also improve livability and secure the home as a future asset. A home with foundation damage could lose one-third of its market value. That would be $100,000 lost on a $300,000 home. If a foundation is sinking or cracking, it could require the major repair of anchoring the home to underground bedrock. This can help homeowners avoid the loss in real estate value while also correcting ongoing issues such as water problems, sagging floors, cracking walls, and pests.

How Has COVID-19 Affected Homeowner Preparedness?

Savings accounts and emergency funds can be quickly depleted. Many people had already used about half of their savings to cover expenses during the pandemic, according to a September 2020 report from investment analysts at Motley Fool. The median savings account balance is now $3,500.

During COVID-19. household income may have been disrupted, and expenses such as childcare may have gone up. Yet households may have saved money on fewer trips to restaurants or canceled vacation plans.

The financial reshuffling has caused about one-third of homeowners to use money from canceled vacations to pay for home repairs. More than half of these homeowners are focusing on structural home repairs.

This tells us that homeowners are investing in repairs that are a good long-term value.

What Can Property Owners Do to Protect Their Homes?

In many cases, small steps for prevention and mitigation can help homeowners avoid the large emergency repairs that top $10,000.

This principle applies to all areas of the home. For example, HVAC maintenance can help extend the life of the furnace and air conditioning system. Homeowners can also remove tree limbs that threaten the roof and address vegetation or drainage issues that could be harming the foundation.

Inside the home, water mitigation systems in a basement or crawl space are an important way to prevent flood damage. Sump pumps, interior drainage, dehumidifiers, and flood vents are valuable investments that have a lasting benefit in mitigating major repairs.

Water management systems are so important that many flood insurance plans will chip in $1,000 per year toward homeowner repairs such as installing sump pumps.

Does your home have structural problems or water issues? Get a free inspection from the country’s leading basement waterproofing and foundation repair experts to learn what it would take to protect your home.